If you work with time series data, you need to know moving average models. I’m going to show you some basic related R commands.

set.seed(123)

# Simulate 250 observations from the described MA(1) model

ma1_sim = arima.sim(model = list(ma=0.5), n=250, mean=0, sd=0.1) + 0.05

ma2_sim = arima.sim(model = list(ma=0.9), n=250, mean=0, sd=0.1) + 0.05

# Generate the theoretical ACF with upto lag 10

acf_ma1_model = ARMAacf(ma=0.5, lag.max=10)

acf_ma2_model = ARMAacf(ma=0.9, lag.max=10)

# Split plotting window in three rows

par(mfrow=c(3,1))

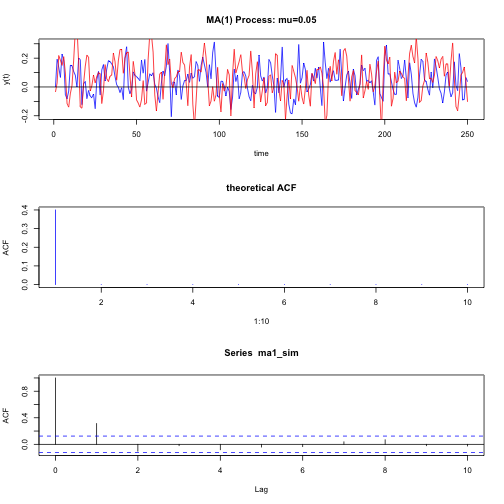

# First plot: The simulated observations

plot(ma1_sim, type="l", main="MA(1) Process: mu=0.05",

xlab="time", ylab="y(t)", col="blue")

lines(ma2_sim, type="l", col="red")

abline(h=0)

# Second plot: Theoretical ACF

plot(1:10, acf_ma1_model[2:11], type="h", col="blue", ylab="ACF",

main="theoretical ACF")

# Third plot: Sample ACF

tmp = acf(ma1_sim, lag.max=10) # Assign to tmp the Sample ACF

str(tmp)## List of 6

## $ acf : num [1:11, 1, 1] 1 0.3133 -0.1035 -0.0206 -0.0818 ...

## $ type : chr "correlation"

## $ n.used: int 250

## $ lag : num [1:11, 1, 1] 0 1 2 3 4 5 6 7 8 9 ...

## $ series: chr "ma1_sim"

## $ snames: NULL

## - attr(*, "class")= chr "acf"# Reset graphical window to only one graph

par(mfrow=c(1,1))